I was looking over my posts from the past year and I'm pleased that my prediction record wasn't so bad. Unfortunately, however, it's looking like my worst call will end up being my most recent one - that the fiscal cliff would be averted. I still think it'll play out in a way favorable to Dem policy priorities, but after Boehner's debacle Thursday night, I'm not so confident a deal will be reached before 12/31, if only because it appears there's too many GOP Representatives who can't vote for anything that has the appearance of a tax increase. To that, I would note that timing is everything: while Obama's offer is a big tax hike relative to current policy, as of Jan. 1 a vote in its favor would actually be a vote to cut taxes. As b.s. as that sounds, the distinction may be important to Republican representatives who have gerrymandered themselves into ideological straitjackets.

The other prediction I wanted to mention was my argument this time last year for US stocks as a good long term investment. The market is up double digits since then, but what I really wanted to point out is that my most important argument, that relative income yields indicated that stocks were cheaper than bonds, is still true. So if the fiscal cliff noise causes some big market gyrations, long term investors could do worse than take advantage of the buying opportunity.

Finally, while it's useful to take stock of the past year, it's also worthwhile to zoom out further, because in so doing you may appreciate that despite the wall of worry our economy is climbing and the insanity of our political culture, and despite the occasional heartbreaking tragedy, the basic measures of humanity's progress are moving in the right direction and at a decent clip, too:

1. People are living longer than ever - even in North Korea!

2. The number of people living in extreme poverty has been cut in half since 1990 - the upside of a globalized economy?

3. The world is a far less violent place than it pretty much ever has been. 'nuff said!

I'm not saying we don't have big problems, just that while there's been a lot to fret over these past few years, in the grand scheme of things there's good cause for optimism.

Saturday, December 22, 2012

Saturday, November 17, 2012

Fiscal cliff prediction: Dems will prevail

People are wondering what will happen as we approach the fiscal cliff. Neither side wants to go over it, but how can they come to an agreement? Political analysts debate the election outcome and who has what kind of mandate. The analysis gets murky, because both sides have arguments that the election ratified their position - Obama won, but GOP retained the House.

Some people look to game theory for clues on how this might play out. I've read several analyses that liken the situation to a game of chicken. Think of "Rebel Without a Cause," where the two teens are driving cars straight for a cliff, and the first one to "chicken out" is the loser. This is obviously not a great game to find yourself playing, because it's very possible that not losing could also mean not surviving.

But thinking of the fiscal cliff negotiation as a game of chicken is dead wrong, because a necessary precondition of the chicken game is that shooting off the cliff is an equally undesirable outcome for each player, and that's not the case with the fiscal cliff.

The way I see it, there are 5 basic consequences of our going over the fiscal cliff, each with varying degrees of alignment to the parties' policy objectives:

1. Analysts say the cliff will cause a recession: no one wants this to happen.

2. Tax rates of rich people will rise: Good for Dems, bad for GOP.

3. Tax rates of regular people will rise: no one wants this to happen.

4. Defense spending will be slashed: Good for Dems, bad for GOP.

5. Non-defense discretionary spending will be slashed: Bad for Dems, Good for GOP.

So, no one wants #1 and #3 to happen, but Dems want to see #2 and #4, while GOP only gains from #5. In my admittedly simplistic scoring, Dems win, 2-1.

The great game theorist John Nash provided a very simple means for predicting the outcome of a negotiation, which boils down to this: whoever has less to lose from a breakdown in talks will wring the most from their opponent. From a policy perspective, it's clear that the Democrats have the least to lose from going off the cliff and therefore the most likely outcome is that the two sides will reach an agreement to avert the cliff and the terms of the agreement will favor the Dems, though probably not without at least some compromise along the way.

Of course, just because the Dems have the upper hand doesn't mean they won't misplay it somehow. Many liberals feel like Obama has a poor track record in negotiating with Republicans. I have the exact opposite view, as evidenced by the simple fact that those earlier negotiations have led us to this scenario where the rules are so clearly tilted in his favor. Game, set, and match.

Some people look to game theory for clues on how this might play out. I've read several analyses that liken the situation to a game of chicken. Think of "Rebel Without a Cause," where the two teens are driving cars straight for a cliff, and the first one to "chicken out" is the loser. This is obviously not a great game to find yourself playing, because it's very possible that not losing could also mean not surviving.

But thinking of the fiscal cliff negotiation as a game of chicken is dead wrong, because a necessary precondition of the chicken game is that shooting off the cliff is an equally undesirable outcome for each player, and that's not the case with the fiscal cliff.

The way I see it, there are 5 basic consequences of our going over the fiscal cliff, each with varying degrees of alignment to the parties' policy objectives:

1. Analysts say the cliff will cause a recession: no one wants this to happen.

2. Tax rates of rich people will rise: Good for Dems, bad for GOP.

3. Tax rates of regular people will rise: no one wants this to happen.

4. Defense spending will be slashed: Good for Dems, bad for GOP.

5. Non-defense discretionary spending will be slashed: Bad for Dems, Good for GOP.

So, no one wants #1 and #3 to happen, but Dems want to see #2 and #4, while GOP only gains from #5. In my admittedly simplistic scoring, Dems win, 2-1.

The great game theorist John Nash provided a very simple means for predicting the outcome of a negotiation, which boils down to this: whoever has less to lose from a breakdown in talks will wring the most from their opponent. From a policy perspective, it's clear that the Democrats have the least to lose from going off the cliff and therefore the most likely outcome is that the two sides will reach an agreement to avert the cliff and the terms of the agreement will favor the Dems, though probably not without at least some compromise along the way.

Of course, just because the Dems have the upper hand doesn't mean they won't misplay it somehow. Many liberals feel like Obama has a poor track record in negotiating with Republicans. I have the exact opposite view, as evidenced by the simple fact that those earlier negotiations have led us to this scenario where the rules are so clearly tilted in his favor. Game, set, and match.

Thursday, October 11, 2012

Open the gates

Conservative economist Casey Mulligan points out on the New York Times econ blog that many worried labor market analysts overlook the impact of the retirement of the baby boomers on our labor force. All things being equal, the percentage of our population that hold jobs will decline as the Woodstock generation tunes out. To that, I say:

It is surprising that all these eyes on the employment situation don't see the rather obvious, and it's equally surprising that many who do don't extend the thought to consider the implications, namely the profound drag on growth a graying population represents. Fewer taxpayers covering the needs of more retirees.

This to me is the central argument for liberalizing immigration. Simply put, our economy acts in some ways like a gigantic Ponzi scheme and we're at a point where we need some new investors to cover the folks cashing out. We also need to figure out how make our economy less Ponzi-like (e.g., improve the efficiency of our healthcare spending), but the least painful way to avoid the real fiscal cliff we all should be worried about is to import more younger people.

It is surprising that all these eyes on the employment situation don't see the rather obvious, and it's equally surprising that many who do don't extend the thought to consider the implications, namely the profound drag on growth a graying population represents. Fewer taxpayers covering the needs of more retirees.

This to me is the central argument for liberalizing immigration. Simply put, our economy acts in some ways like a gigantic Ponzi scheme and we're at a point where we need some new investors to cover the folks cashing out. We also need to figure out how make our economy less Ponzi-like (e.g., improve the efficiency of our healthcare spending), but the least painful way to avoid the real fiscal cliff we all should be worried about is to import more younger people.

Wednesday, September 12, 2012

A comment on the new fuel efficiency standards

Dear Mr. Porter,

I appreciate the interesting article in today's Times in which you challenge the efficacy of the new fuel efficiency standards, but I have to take issue with the outdated argument that a domestic gas tax would more efficiently reduce consumption. Unfortunately, the Times does not allow for reader comments on Economic Scene articles, so I am sending this directly to you instead [and apparently posting it to my blog]. The crux of the counterargument is that since oil is now a truly global market, any reduction in US consumption caused by local factors (such as a domestic tax) would be offset by increased foreign consumption brought on by a lower global price (caused by lower US demand due to the higher domestic price).

At this point the only oil tax that would actually reduce consumption would have to be applied globally. Nevertheless, conservationists can look forward to the tax-like effect of what is likely to be a long-running trend of upward price pressure exerted by the rapidly growing middle class in Brazil, China, India and other emerging markets. In this context and contrary to the thrust of your article, raising domestic fuel efficiency standards (which in regulating the world's 2nd largest car market will likely improve standards globally) is perhaps the only effective unilateral action available to the Obama administration.

Yours truly,

Jake Tamarkin

p.s. For more on the effect of local oil taxes on global consumption, please see my blog post on a related article by the esteemed William Nordhaus:

http://jaketamarkin.blogspot.com/2011/11/letter-new-york-review-of-books-didnt.html

I appreciate the interesting article in today's Times in which you challenge the efficacy of the new fuel efficiency standards, but I have to take issue with the outdated argument that a domestic gas tax would more efficiently reduce consumption. Unfortunately, the Times does not allow for reader comments on Economic Scene articles, so I am sending this directly to you instead [and apparently posting it to my blog]. The crux of the counterargument is that since oil is now a truly global market, any reduction in US consumption caused by local factors (such as a domestic tax) would be offset by increased foreign consumption brought on by a lower global price (caused by lower US demand due to the higher domestic price).

At this point the only oil tax that would actually reduce consumption would have to be applied globally. Nevertheless, conservationists can look forward to the tax-like effect of what is likely to be a long-running trend of upward price pressure exerted by the rapidly growing middle class in Brazil, China, India and other emerging markets. In this context and contrary to the thrust of your article, raising domestic fuel efficiency standards (which in regulating the world's 2nd largest car market will likely improve standards globally) is perhaps the only effective unilateral action available to the Obama administration.

Yours truly,

Jake Tamarkin

p.s. For more on the effect of local oil taxes on global consumption, please see my blog post on a related article by the esteemed William Nordhaus:

http://jaketamarkin.blogspot.com/2011/11/letter-new-york-review-of-books-didnt.html

Sunday, August 19, 2012

How Bush killed the Left

It's not news that Bush the Younger is not held in high regard. One recent poll shows that he is the least popular of the living ex-presidents, the only one with a sub 50% approval rating. The GOP knows this, and his absence from the campaign trail contrasts sharply with Bill Clinton's activism.

This masks an important point: Bush has done more to advance the libertarian cause than any other single person. His truly spectacular mismanagement convinced people across the political spectrum that Reagan was right, "government isn't the solution to our problem: it's the problem." While Grover Norquist aligned the GOP around the mission of shrinking government to where they could "drown it in a bathtub," it was Bush who got the rubber to meet the road by disillusioning the broader electorate -including the far left- to the point where they have wholly abandoned the premise that government is good. Consider the following two excerpts from a 2011 Gallup report titled "Americans Express Historic Negativity Toward U.S. Government":

1. "A record-high 81% of Americans are dissatisfied with the way the country is being governed, adding to negativity that has been building for the past 10 years."

2. "Americans believe, on average, that the federal government wastes 51 cents of every tax dollar...up significantly from 46 cents a decade ago, and from an average 43 cents three decades ago."

Game, set, and match. In a future post, I'll explore the enormity of this to the progressive movement. Or maybe not. Why bother? (damn - get him out of my head!)

This masks an important point: Bush has done more to advance the libertarian cause than any other single person. His truly spectacular mismanagement convinced people across the political spectrum that Reagan was right, "government isn't the solution to our problem: it's the problem." While Grover Norquist aligned the GOP around the mission of shrinking government to where they could "drown it in a bathtub," it was Bush who got the rubber to meet the road by disillusioning the broader electorate -including the far left- to the point where they have wholly abandoned the premise that government is good. Consider the following two excerpts from a 2011 Gallup report titled "Americans Express Historic Negativity Toward U.S. Government":

1. "A record-high 81% of Americans are dissatisfied with the way the country is being governed, adding to negativity that has been building for the past 10 years."

2. "Americans believe, on average, that the federal government wastes 51 cents of every tax dollar...up significantly from 46 cents a decade ago, and from an average 43 cents three decades ago."

Game, set, and match. In a future post, I'll explore the enormity of this to the progressive movement. Or maybe not. Why bother? (damn - get him out of my head!)

Saturday, July 21, 2012

You didn't build that. No, really.

Is the US a meritocracy? This chart, lifted from a fascinating OECD paper on social mobility, seems to suggest otherwise, because in a meritocracy your birthright should be less predictive of your destiny, and we're showing up behind such objects of libertarian scorn as France, Germany, Sweden and Canada (Canada!):

This is relevant to our current political debate because Romney is trying to make hay off of Obama's comments to this effect (the "you didn't build that" kerfuffle). As opposed to most of the campaign noise - I pity swing state tv watchers - this particular debate is actually important.

Romney argues for what amounts to economic elitism, where tax policy favors "job creators" (aka rich people). Obama argues for essentially a means-based taxation system. Both are predicated on the principle that our system should be funded by the people that benefit most from it; the difference is in who you perceive to be its primary beneficiaries.

The argument I've made previously on this blog is that rich people benefit more from our government than poor people, and the logic is simple: if government isn't a key enabler of wealth creation, then relatively lawless places should be comparative hotbeds of innovation and "job creation". So, what do you imagine is the unemployment rate in, say, Somalia? 75%, according to this UN study. What?!? Where are my job creators at? It's an extreme example, but it helps make the point that the value you get from the enforcement of property rights, to name but one governmental function, is commensurate with the value of your property.

Republican orthodoxy counters that the more we make the rich pay in taxes, the less incentive we give people to strive to better their economic situation; that is, that the best way to promote a meritocracy is to increase the rewards of success. At this point we should refer back to the chart at the top of this post, which essentially suggests that rather than spend our resources encouraging people to want to improve their lot (never met someone that needed encouragement on this front, btw), we can best promote meritocratic principles by helping those who didn't win the birth lottery.

Saturday, June 30, 2012

Updated look at income and savings: in which I eat crow

The Bureau of Economic Analysis released their first view of May's economic activity yesterday and also revised their Jan-April numbers, too. Unfortunately, the update is not entirely consistent with the view I offered last week, and so I must revise my analysis (please pass the crow). Here's an updated view of the same chart I showed you last week, limited to just the more recent months:

If you'll recall, my take before was that, with consumers' buying power rising and their savings rates falling, consumption would accelerate and thus the fears of a slowdown in our recovery were unfounded. This was a contrarian view to what we've been hearing about job growth stalling and consumer sentiment souring. However, the updated data shows that while buying power is indeed picking up steam, so has the savings rate.

The rise in savings rate is consistent with several recent surveys that have suggested that consumers are less optimistic than they were a few months ago. My interpretation was that the surveys were less meaningful than the savings data, because money speaks louder than words (call it the Bobbi Fleckman principle). Still, the income gains don't reflect a basis for the relative pessimism. Even if you look at buying power on a per capita basis, things are clearly getting better:

Ok, so maybe the nice 3-month run we're on will later get revised down. Or maybe consumers take longer to acknowledge the improvements and they'll perk up over the summer. Or maybe the improvements are too mild to overshadow the b.s. you hear on the news. Who knows, but I do believe there is a slight disconnect between reality and our perception of it. Or maybe my perception of it. Pass the ketchup.

Ok, so maybe the nice 3-month run we're on will later get revised down. Or maybe consumers take longer to acknowledge the improvements and they'll perk up over the summer. Or maybe the improvements are too mild to overshadow the b.s. you hear on the news. Who knows, but I do believe there is a slight disconnect between reality and our perception of it. Or maybe my perception of it. Pass the ketchup.

|

| Source: Bureau of Economic Analysis |

The rise in savings rate is consistent with several recent surveys that have suggested that consumers are less optimistic than they were a few months ago. My interpretation was that the surveys were less meaningful than the savings data, because money speaks louder than words (call it the Bobbi Fleckman principle). Still, the income gains don't reflect a basis for the relative pessimism. Even if you look at buying power on a per capita basis, things are clearly getting better:

Wednesday, June 20, 2012

The stability of the recovery

First, let me apologize for being away for so long. Work got busy and then I was overwhelmed by an apartment hunt (still am, in fact). It occurs to me that if everyone were busy with work and buying real estate then I suppose I wouldn't need to be making a case for optimism, nor would anyone be reading it, but that's not quite where we are, are we?

If you follow economic news, then when you aren't deluged with hand-wringing over Europe, you're getting slammed with worries over the recent jobs numbers. My take on Europe's influence on our economy is essentially unchanged since I last posted about it, so I am going to focus on the jobs concern. Employers don't seem to be adding jobs at a pace necessary to put everyone back to work within a reasonable amount of time. But as disturbing as this is, it doesn't mean we're headed toward another recession. For one thing, jobs lag demand (employers don't hire extra help until they can't keep up with customer demand) and consumer demand growth is steady, if unspectacular. Meanwhile, improvements in consumer sentiment and buying power suggest that it's reasonable to expect demand growth to accelerate modestly going forward.

Ok, I know this chart is ridiculous, but bear with me.

The solid blue line is showing changes in the total disposable income of US consumers from January, 2007 through April, 2012. It has been adjusted for inflation, so it is a good measure of consumer buying power - as the line goes up, consumers are collectively able to buy more stuff than they were before, and as the line goes down either inflation is rising or income is declining, or some combination of the two is taking place.

The red dotted line represents the consumer savings rate, defined as the percentage of disposable income that isn't spent. There are different reasons why this can fluctuate over time, but one of them certainly is consumer sentiment. If you are pessimistic about your financial future, you are likely to try to save more, and the opposite is true - if you feel relatively secure, there is less of a sense of urgency to prepare for seemingly unlikely bad times. So, it's fairly intuitive to appreciate how consumer spending is a function of these two factors; meanwhile, a review of how they have fluctuated in recent years lends insight into our prospects.

Consider the shaded period (1). This corresponds roughly with the last recession, and it's plain to see that not only was buying power lower at the end of the recession than it was at the beginning, but also the savings rate ends the recession higher. (By the way, if you're curious about that income spike in early 2008, that was Bush's emergency stimulus tax rebates he sent out. It's interesting to note that the savings rate spiked along with it, indicating that people chose to save the rebate rather than spend it, which is entirely consistent with how you would expect a pessimistic populace to behave.) These trends are precisely what we should expect to see: bad times were occasioned by - if not defined by - a drop in buying power, and we collectively responded by getting more conservative in our spending habits. Indeed, almost half of the drop in consumer spending during the recession can be attributed to the increased savings rate.

Now look at the second shaded period (2), basically representing the last two years, where we see the opposite happened. Buying power rose slowly but surely, and the savings rate dropped like a stone. This is likewise intuitive; as our situation improved, we loosened the purse strings. Analyzing the consumer spending gains during this period, it's interesting that fully 60% of the increased consumer spending over the last two years was due to brightening consumer sentiment as articulated in the drop in the savings rate.

What does all this mean going forward? One conclusion we can easily draw is that, now that the savings rate is more-or-less back down to pre-recession levels, each additional dollar of buying power will generate more consumer spending than it did previously. So, to the extent we base our expectations on recent history (as the so-called conventional wisdom often tends to do), we will underestimate the effect even modest increases in buying power will have on consumer demand and, eventually, on job growth.

If you follow economic news, then when you aren't deluged with hand-wringing over Europe, you're getting slammed with worries over the recent jobs numbers. My take on Europe's influence on our economy is essentially unchanged since I last posted about it, so I am going to focus on the jobs concern. Employers don't seem to be adding jobs at a pace necessary to put everyone back to work within a reasonable amount of time. But as disturbing as this is, it doesn't mean we're headed toward another recession. For one thing, jobs lag demand (employers don't hire extra help until they can't keep up with customer demand) and consumer demand growth is steady, if unspectacular. Meanwhile, improvements in consumer sentiment and buying power suggest that it's reasonable to expect demand growth to accelerate modestly going forward.

Ok, I know this chart is ridiculous, but bear with me.

The solid blue line is showing changes in the total disposable income of US consumers from January, 2007 through April, 2012. It has been adjusted for inflation, so it is a good measure of consumer buying power - as the line goes up, consumers are collectively able to buy more stuff than they were before, and as the line goes down either inflation is rising or income is declining, or some combination of the two is taking place.

The red dotted line represents the consumer savings rate, defined as the percentage of disposable income that isn't spent. There are different reasons why this can fluctuate over time, but one of them certainly is consumer sentiment. If you are pessimistic about your financial future, you are likely to try to save more, and the opposite is true - if you feel relatively secure, there is less of a sense of urgency to prepare for seemingly unlikely bad times. So, it's fairly intuitive to appreciate how consumer spending is a function of these two factors; meanwhile, a review of how they have fluctuated in recent years lends insight into our prospects.

Consider the shaded period (1). This corresponds roughly with the last recession, and it's plain to see that not only was buying power lower at the end of the recession than it was at the beginning, but also the savings rate ends the recession higher. (By the way, if you're curious about that income spike in early 2008, that was Bush's emergency stimulus tax rebates he sent out. It's interesting to note that the savings rate spiked along with it, indicating that people chose to save the rebate rather than spend it, which is entirely consistent with how you would expect a pessimistic populace to behave.) These trends are precisely what we should expect to see: bad times were occasioned by - if not defined by - a drop in buying power, and we collectively responded by getting more conservative in our spending habits. Indeed, almost half of the drop in consumer spending during the recession can be attributed to the increased savings rate.

Now look at the second shaded period (2), basically representing the last two years, where we see the opposite happened. Buying power rose slowly but surely, and the savings rate dropped like a stone. This is likewise intuitive; as our situation improved, we loosened the purse strings. Analyzing the consumer spending gains during this period, it's interesting that fully 60% of the increased consumer spending over the last two years was due to brightening consumer sentiment as articulated in the drop in the savings rate.

What does all this mean going forward? One conclusion we can easily draw is that, now that the savings rate is more-or-less back down to pre-recession levels, each additional dollar of buying power will generate more consumer spending than it did previously. So, to the extent we base our expectations on recent history (as the so-called conventional wisdom often tends to do), we will underestimate the effect even modest increases in buying power will have on consumer demand and, eventually, on job growth.

Sunday, April 8, 2012

blaming the banks

People are still pissed at the banks for screwing us all over and this anger is horribly misplaced. It's like blaming the bartender for your hangover, and it's disturbing to think we may be learning the wrong lessons from this whole economic debacle. Consider the chart below, which shows that in the decade leading up to the Great Recession, the average person's debt grew at a rate roughly twice as fast as their income:

It's pretty easy to see the connection between this debt run-up and the economic collapse, but did the banks force us to borrow beyond our means? Did the bartender force us to chug down those extra shots? Many states have laws that restrict bartenders from serving obviously drunk people, and likewise our financial system used to have reasonably effective safeguards against these kinds of excesses. But they were dismantled by anti-regulatory zealots in the 1980s, 1990s, and 2000s. Who kept voting these people into power?

Similarly, there is a widespread misunderstanding about why we bailed out the banks. Some people smell a conspiracy but this overlooks the simple truth that we did it to save ourselves. If the local nuclear power plant started overheating beyond the control of its managers, it would be a no-brainer to send in public safety resources to prevent a meltdown that could ruin the surrounding communities. It was a similar concern that motivated the bailout of the banks. Our financial power system is as potent as our electrical power system and should be regulated accordingly.

But while re-regulating the financial system deals with the proximate cause of imprudent banking practices, it misses entirely the ultimate cause of out of control consumer debt. Why were people borrowing so far beyond what they could afford? As I argue in my Jan. 4 post ("Dirty Money"), I believe it was due in part to the Reagan and Bush II tax cuts that disproportionately favored the wealthiest and increased income inequality. In his timely, if tragically under-appreciated, 2007 book "Falling Behind: How Inequality Harms the Middle Class", the great economist Bob Frank argues that a good deal of consumer spending is positional - that is, much of it is aimed at gaining a competitive advantage in the great Darwinian game that is life on earth. For example, only half of our children can have an above-average education, so a scenario where the wealthiest bid up homes in the best school districts forces everyone else to spend more so as not to fall behind.

Sure, bankers behaved badly, but any worse than the rest of us who backed this ideology with our political support? Besides, the bankers' behavior was entirely predictable - the fact that many of the regulations we dismantled were themselves antidotes to the Great Depression puts such moves squarely into the "fool me twice, shame on me" category. Bottom line: to scapegoat Wall Street is to deny our own culpability and the fact that the GOP is still peddling these so thoroughly discredited ideas and the magical thinking they require only highlights the importance of getting our facts straight. We've already paid a heavy price for our schooling, so let's make sure we learn the right lessons: progressive taxes and responsible regulation are cornerstones of our prosperity.

It's pretty easy to see the connection between this debt run-up and the economic collapse, but did the banks force us to borrow beyond our means? Did the bartender force us to chug down those extra shots? Many states have laws that restrict bartenders from serving obviously drunk people, and likewise our financial system used to have reasonably effective safeguards against these kinds of excesses. But they were dismantled by anti-regulatory zealots in the 1980s, 1990s, and 2000s. Who kept voting these people into power?

Similarly, there is a widespread misunderstanding about why we bailed out the banks. Some people smell a conspiracy but this overlooks the simple truth that we did it to save ourselves. If the local nuclear power plant started overheating beyond the control of its managers, it would be a no-brainer to send in public safety resources to prevent a meltdown that could ruin the surrounding communities. It was a similar concern that motivated the bailout of the banks. Our financial power system is as potent as our electrical power system and should be regulated accordingly.

But while re-regulating the financial system deals with the proximate cause of imprudent banking practices, it misses entirely the ultimate cause of out of control consumer debt. Why were people borrowing so far beyond what they could afford? As I argue in my Jan. 4 post ("Dirty Money"), I believe it was due in part to the Reagan and Bush II tax cuts that disproportionately favored the wealthiest and increased income inequality. In his timely, if tragically under-appreciated, 2007 book "Falling Behind: How Inequality Harms the Middle Class", the great economist Bob Frank argues that a good deal of consumer spending is positional - that is, much of it is aimed at gaining a competitive advantage in the great Darwinian game that is life on earth. For example, only half of our children can have an above-average education, so a scenario where the wealthiest bid up homes in the best school districts forces everyone else to spend more so as not to fall behind.

Sure, bankers behaved badly, but any worse than the rest of us who backed this ideology with our political support? Besides, the bankers' behavior was entirely predictable - the fact that many of the regulations we dismantled were themselves antidotes to the Great Depression puts such moves squarely into the "fool me twice, shame on me" category. Bottom line: to scapegoat Wall Street is to deny our own culpability and the fact that the GOP is still peddling these so thoroughly discredited ideas and the magical thinking they require only highlights the importance of getting our facts straight. We've already paid a heavy price for our schooling, so let's make sure we learn the right lessons: progressive taxes and responsible regulation are cornerstones of our prosperity.

Sunday, March 4, 2012

How much should we be worried about rising gasoline prices?

That the recovery has taken root is now a well-established story in the mainstream media, so I was going to move on to other subjects but the recent coverage of rising gasoline prices and its economic and political implications seemed to be nearing a hysterical pitch, so I thought I should look into it.

Simply put, there is no relationship between oil prices and economic growth. (Statistics nerds will appreciate that my regression analysis of quarterly changes in real GDP against oil prices from January, 1947 - January, 2012 showed a correlation of 0.08, R-squared 0.006, and a standard error almost exactly the same as GDP's standard deviation. Further, I was unable to find any 10-year period in that span that featured a discernible connection between the two.) This is due in part to the fact that the energy industry is a major contributor to our economy. Beyond that, and perhaps contrary to conventional wisdom, it could be argued at this point rising energy prices are beneficial to our aggregate economic growth because we are once again net exporters of petroleum products. And in the short run it's not hard to imagine that steeply rising gas prices would accelerate the process of people catching up on automobile purchases they had deferred during the downturn.

So what's the big deal? The issue the pundits are wringing their hands over (and just about anyone who's had to buy a tank of unleaded gas understands) is that higher oil prices can divert consumer spending away from the things people really value (e.g., food, shelter, entertainment). But how much? To get an idea, it's helpful to look at energy spending's place in our collective household budgets and how that's changed over time:

A couple of observations:

1. There is a distinct long-run downtrend of energy's role in our budgets. This is consistent with the notion that over time we've become more efficient energy consumers.

2. The two big deviations from the trendline relate to the two most significant periods of oil price volatility: roughly 1974-1986 and 1999-now. The 1974-1986 period pretty much follows the same contour as oil prices, indicating that the oil price changes didn't affect our energy consumption as much as it crowded out spending on other things. This is the kind of painful displacement that political pundits think could derail Obama's prospects.

But a closer look at what's been going on since 1999 reveals a different story:

The period begins at 4%, the lowest level on record, peaks at 7% in 2008 (when oil spiked to almost $140/barrel) and ends at about 5.5%, just above the 5.25% average for the period. While the line broadly tracks oil prices, the slope tends to be much more gradual. This is very different from what we saw during the oil price shock of the 1970's.

Consumers' budgets are clearly less sensitive to oil price swings than they used to be, and there several reasons, including our diversification of energy sources (natural gas recently became the #1 home heating fuel) and efficiency improvements to our transportation. But perhaps most significant is the simple fact that we don't drive as much as we used to:

This chart shows per capita miles driven in the US since 1970. It's easy to see that we've driven fewer miles on average since the 2004 peak, but it's also noteworthy that the rate of growth prior to then was declining, too. In the 1970s and 1980s, per capita driving was growing at a 2.4% average annual rate, but the rate shrank to less than half that in the 1990s and up until the 2004 peak (1.15%). I could only guess as to why, but it's reasonable to imagine that it's at least partially due to the proliferation of the internet - there is so much stuff we do online that our parents used to have to leave the house to do (banking, shopping, working, etc.).

All of this is just to say that fears that a spike in gas prices will sink either our economy or Obama's prospects are way overblown. There is no evidence that higher energy prices actually damage our economy, and while no driver likes to see higher gas prices, it's not as big a deal as it used to be.

Simply put, there is no relationship between oil prices and economic growth. (Statistics nerds will appreciate that my regression analysis of quarterly changes in real GDP against oil prices from January, 1947 - January, 2012 showed a correlation of 0.08, R-squared 0.006, and a standard error almost exactly the same as GDP's standard deviation. Further, I was unable to find any 10-year period in that span that featured a discernible connection between the two.) This is due in part to the fact that the energy industry is a major contributor to our economy. Beyond that, and perhaps contrary to conventional wisdom, it could be argued at this point rising energy prices are beneficial to our aggregate economic growth because we are once again net exporters of petroleum products. And in the short run it's not hard to imagine that steeply rising gas prices would accelerate the process of people catching up on automobile purchases they had deferred during the downturn.

So what's the big deal? The issue the pundits are wringing their hands over (and just about anyone who's had to buy a tank of unleaded gas understands) is that higher oil prices can divert consumer spending away from the things people really value (e.g., food, shelter, entertainment). But how much? To get an idea, it's helpful to look at energy spending's place in our collective household budgets and how that's changed over time:

A couple of observations:

1. There is a distinct long-run downtrend of energy's role in our budgets. This is consistent with the notion that over time we've become more efficient energy consumers.

2. The two big deviations from the trendline relate to the two most significant periods of oil price volatility: roughly 1974-1986 and 1999-now. The 1974-1986 period pretty much follows the same contour as oil prices, indicating that the oil price changes didn't affect our energy consumption as much as it crowded out spending on other things. This is the kind of painful displacement that political pundits think could derail Obama's prospects.

But a closer look at what's been going on since 1999 reveals a different story:

The period begins at 4%, the lowest level on record, peaks at 7% in 2008 (when oil spiked to almost $140/barrel) and ends at about 5.5%, just above the 5.25% average for the period. While the line broadly tracks oil prices, the slope tends to be much more gradual. This is very different from what we saw during the oil price shock of the 1970's.

Consumers' budgets are clearly less sensitive to oil price swings than they used to be, and there several reasons, including our diversification of energy sources (natural gas recently became the #1 home heating fuel) and efficiency improvements to our transportation. But perhaps most significant is the simple fact that we don't drive as much as we used to:

This chart shows per capita miles driven in the US since 1970. It's easy to see that we've driven fewer miles on average since the 2004 peak, but it's also noteworthy that the rate of growth prior to then was declining, too. In the 1970s and 1980s, per capita driving was growing at a 2.4% average annual rate, but the rate shrank to less than half that in the 1990s and up until the 2004 peak (1.15%). I could only guess as to why, but it's reasonable to imagine that it's at least partially due to the proliferation of the internet - there is so much stuff we do online that our parents used to have to leave the house to do (banking, shopping, working, etc.).

All of this is just to say that fears that a spike in gas prices will sink either our economy or Obama's prospects are way overblown. There is no evidence that higher energy prices actually damage our economy, and while no driver likes to see higher gas prices, it's not as big a deal as it used to be.

Thursday, March 1, 2012

Income update

I mentioned in my last post that it would be worthwhile to look out for the March 1 report on personal income earned in January. Below is an update of the chart from my last post, where the focus is on personal income associated with business payrolls (as opposed to personal income from government sources or investment earnings). There are 2 noteworthy developments:

1. The Bureau of Economic Analysis revised upward their #'s for 3rd & 4th quarter 2011.

2. January's gains were roughly on par with December's.

Taken together, this should make us more confident in the sustainability of our economic recovery. Steady gains to personal income earned from private payrolls is the healthiest enabler of growth in consumer spending, and consumer spending is what ultimately drives our economy.

1. The Bureau of Economic Analysis revised upward their #'s for 3rd & 4th quarter 2011.

2. January's gains were roughly on par with December's.

Taken together, this should make us more confident in the sustainability of our economic recovery. Steady gains to personal income earned from private payrolls is the healthiest enabler of growth in consumer spending, and consumer spending is what ultimately drives our economy.

Tuesday, February 21, 2012

Does the recovery have legs? Part 2: The income strikes back

I think the single most important indicator to predict our near-term economic growth is personal income growth. This follows from my previous posts, where I suggest that consumer spending is the key to our recovery, and it's no great insight to suggest that for spending to grow, income must grow. This is particularly true in an environment like ours, where consumers are generally over-indebted and therefore are less likely to use debt to increase spending.

This chart shows growth in compensation people receive from private businesses. This is strictly private wages - that is, I've excluded things like the income of government employees, investment earnings, income from social security and other government programs, and indirect compensation like employer pension contributions. The idea is to specifically focus on the personal income most sensitive to our growth trajectory: the payrolls of businesses.

The story this tells is something of a mixed bag. We are not seeing consistent growth over each of the last few months, and what growth there has been is lower than the gains we saw Jan-Feb 2011 or even Mar-May 2010, for that matter. On the other hand, the last 4-5 months overall look better than the 4-5 before them. So, the jury is still out here, which makes it all the more important that we follow this closely over the next few months. The report on January's performance comes out March 1, and we should be looking to see if private compensation grew more or less rapidly than it did in December.

My guess - and it's only a guess - is that the report will show that January's wage growth was good, and I'm basing that on the chart below, which shows that the number of people submitting claims for unemployment insurance has dropped more in the last 8 weeks than in the previous 8 months.

It would stand to reason that if private payrolls are expanding, unemployment compensation claims would decline. However, there are other factors that drive these numbers - for example, maybe people stopped filing claims simply because they exhausted their eligibility - so it's just a speculation, but I'm optimistic.

It would stand to reason that if private payrolls are expanding, unemployment compensation claims would decline. However, there are other factors that drive these numbers - for example, maybe people stopped filing claims simply because they exhausted their eligibility - so it's just a speculation, but I'm optimistic.

This chart shows growth in compensation people receive from private businesses. This is strictly private wages - that is, I've excluded things like the income of government employees, investment earnings, income from social security and other government programs, and indirect compensation like employer pension contributions. The idea is to specifically focus on the personal income most sensitive to our growth trajectory: the payrolls of businesses.

The story this tells is something of a mixed bag. We are not seeing consistent growth over each of the last few months, and what growth there has been is lower than the gains we saw Jan-Feb 2011 or even Mar-May 2010, for that matter. On the other hand, the last 4-5 months overall look better than the 4-5 before them. So, the jury is still out here, which makes it all the more important that we follow this closely over the next few months. The report on January's performance comes out March 1, and we should be looking to see if private compensation grew more or less rapidly than it did in December.

My guess - and it's only a guess - is that the report will show that January's wage growth was good, and I'm basing that on the chart below, which shows that the number of people submitting claims for unemployment insurance has dropped more in the last 8 weeks than in the previous 8 months.

Sunday, February 19, 2012

Does the recovery have legs? Part 1: housing on the rebound

It's only been a few months since I became confident enough in our recovery's strength to start blogging about it and it's still tenuous enough to bear close monitoring. But what exactly should we be watching for? One of the great challenges in evaluating economic situations in general is that reality is fluid and it's often hard to distinguish between cause and effect (e.g., are higher wages pushing inflation up or is inflation forcing employers to pay more?). In this and other posts I am going to provide my take.

It's widely understood that the housing market's recovery is key to the sustainability of the broader recovery, and a bird's eye view suggests things are rebounding:

What this chart shows is that in each of the last 3 quarters residential investment has positively contributed to our economic growth, even after adjusting for inflation. And while the contributions were relatively modest as compared to individual quarters in 2009 and 2010, I like to think the consistency of 3 consecutive upticks is meaningful in its own right. I would caution that this simplistic analysis may be missing important considerations, like that a flood of foreclosures on the heels of the recent bank settlement could swamp the market with inventory and depress investment in new construction. Still, after what we've been through it is helpful to see any sign that activity in the most troubled sector of our economy is trending in the right direction.

It's widely understood that the housing market's recovery is key to the sustainability of the broader recovery, and a bird's eye view suggests things are rebounding:

What this chart shows is that in each of the last 3 quarters residential investment has positively contributed to our economic growth, even after adjusting for inflation. And while the contributions were relatively modest as compared to individual quarters in 2009 and 2010, I like to think the consistency of 3 consecutive upticks is meaningful in its own right. I would caution that this simplistic analysis may be missing important considerations, like that a flood of foreclosures on the heels of the recent bank settlement could swamp the market with inventory and depress investment in new construction. Still, after what we've been through it is helpful to see any sign that activity in the most troubled sector of our economy is trending in the right direction.

Sunday, February 12, 2012

The simple case for progressive taxation

It's not enough to make the moral argument that rich people should pay more. A flat tax where everyone pays the same rate accomplishes that much. No, the argument for progressive taxes, that is, a tax structure where higher incomes are taxed at higher rates, is simply that rich people realize a higher rate of return on our public investments and like anything else they should pay what it's worth to them.

I laid this on a friend of mine recently and he almost sprained his neck trying to politely register his dissent. It's counter-intuitive because when we think about how people benefit from public infrastructure we might first think of food stamps and welfare and medicaid (i.e., programs that aid lower income people). But consider this: would Apple exist if Steve Jobs had been born and raised in, say, Yemen?

It's as simple as that.

I laid this on a friend of mine recently and he almost sprained his neck trying to politely register his dissent. It's counter-intuitive because when we think about how people benefit from public infrastructure we might first think of food stamps and welfare and medicaid (i.e., programs that aid lower income people). But consider this: would Apple exist if Steve Jobs had been born and raised in, say, Yemen?

It's as simple as that.

Monday, February 6, 2012

Europe crisis: don't believe the hype about what it means to the US

Washington Post blogger Ezra Klein's morning missive was titled "Obama's Fresh Lead Vulnerable to Europe's Woes," and in it he notes that a Greek debt default would have "untold, but clearly disastrous, consequences for both Europe and the United States." I'm not sure I see it. Maybe we shouldn't leave these consequences as "untold" before we declare them to be "clearly disastrous." To me, the likely fallout doesn't necessarily rise to the level of disaster.

For one thing, according to the EU Trade Commission, in 2010 US exports to the 27 EU nations represented less than 3% of US GDP. Moreover, most of this business is with the stronger nations, like Germany, the Netherlands, and France. Another concern might be that a euro currency collapse would hurt our exports overall, as it would make our products relatively more expensive than European ones, but even still, with all exports representing less than 13% of US GDP in 2010, it would have to be a massive devaluation to really hurt us. This is also an unlikely scenario - for example, if Greece goes down, it's more likely to be booted out of the euro currency altogether rather than degrade it.

To be sure, the crisis in Europe can't be good for us, and their handling of it doesn't give me confidence that it'll be resolved cleanly, but it's far from a no-brainer that it would spark a crisis here. My analysis is admittedly simplistic, but until someone smarter than me takes the time to really think this through we won't have a clear idea until it actually hits the fan. So perhaps the most significant impact is that it's just more bad news that gets amplified by the media and scares people. In other words, maybe the problem here isn't so much that Greece can't pay its bills, it's that too many journalists are taking shortcuts.

UPDATE: 12 hours after this was published, Klein came clean:

"Since I've written many, many Wonkbooks on the threat that Europe poses to America's recovery, it's worth pointing out that there is an increasing number of smart observers downgrading -- if not entirely dismissing -- the continent's importance to the American economy."

For one thing, according to the EU Trade Commission, in 2010 US exports to the 27 EU nations represented less than 3% of US GDP. Moreover, most of this business is with the stronger nations, like Germany, the Netherlands, and France. Another concern might be that a euro currency collapse would hurt our exports overall, as it would make our products relatively more expensive than European ones, but even still, with all exports representing less than 13% of US GDP in 2010, it would have to be a massive devaluation to really hurt us. This is also an unlikely scenario - for example, if Greece goes down, it's more likely to be booted out of the euro currency altogether rather than degrade it.

To be sure, the crisis in Europe can't be good for us, and their handling of it doesn't give me confidence that it'll be resolved cleanly, but it's far from a no-brainer that it would spark a crisis here. My analysis is admittedly simplistic, but until someone smarter than me takes the time to really think this through we won't have a clear idea until it actually hits the fan. So perhaps the most significant impact is that it's just more bad news that gets amplified by the media and scares people. In other words, maybe the problem here isn't so much that Greece can't pay its bills, it's that too many journalists are taking shortcuts.

UPDATE: 12 hours after this was published, Klein came clean:

"Since I've written many, many Wonkbooks on the threat that Europe poses to America's recovery, it's worth pointing out that there is an increasing number of smart observers downgrading -- if not entirely dismissing -- the continent's importance to the American economy."

Tuesday, January 31, 2012

The letter the New Yorker didn't want you to read!

To the Editor:

In “Private Inequity” (January 30), James Surowiecki proposes addressing private-equity’s “financial gimmickry” by capping the deductibility of corporate debt and closing the carried interest loophole. That sounds complicated and politically challenging. Reformers would be better-served by a policy that simply coupled an increase in the capital gains and dividends tax rates with an offsetting reduction in corporate income taxes. It may seem counterintuitive to lower corporate income taxes, but doing so will reduce corporate debt levels because it makes debt more expensive (the lower the tax rate, the lower the value of a deduction). The benefits extend beyond this, however, as it instantly improves the business case for every potential domestic corporate investment, generating immediate stimulus to our economy and permanently tilting the balance away from offshoring jobs. Meanwhile, the offsetting, tax revenue-neutral nature of this approach leaves shareholders unaffected by the change, preempting the Republican concern that higher taxes on capital gains and dividends dampens investment. Moreover, it complements Democratic efforts to raise taxes on wealthy individuals because, to the extent that it encourages businesses to organize as corporations, it disarms the well-worn Republican charge that raising marginal tax rates on individuals hurts otherwise job-creating businesses filing under the individual tax code. For all of these reasons, offsetting higher taxes on capital gains and dividends with lower taxes on corporate income is good policy.

Saturday, January 21, 2012

why we work

"Now is the time to make an adequate income a reality for all God's children. Now is the time for City Hall to take a position for that which is just and honest."

- Dr. Martin Luther King, Jr., addressing striking sanitation workers in Memphis, March 18, 1968

The living wage movement uses MLK's words as a rallying cry to require employers to pay enough for people to get by. A noble aim, but it's an example of how a simplistic view of our role in the economy leads to self-defeating policy. Unfortunately, you shoot yourself in the foot when you target wages.

We should consider why we work in the first place: to pay for the things we need to get by. I can tell you that if everything were free, I wouldn't be a worker at all (if only!). It follows, then, that our interests as consumers should take precedence over our interests as workers, and that we are better served ensuring the adequacy of our income by focusing our efforts on reducing the cost of living rather than increasing our means to meet it. Not only would we more directly address the essential problem at hand, we would avoid the self-defeating aspect of increasing aggregate income, a scenario where the benefit of higher wages is offset by the inflationary pressure pay raises put on production expenses. Your standard of living doesn't improve if your raise is offset by price increases. Lazy people like me appreciate how this dynamic sends us in the wrong direction.

Perhaps this sounds uncomfortably similar to the supply-side economics championed by the right since the days of Reagan. Still, we can't ever let partisanship triumph over reason, and it's a valid observation that we should prefer cutting costs to raising income (if food were free, wouldn't you join me in a life of leisure?). The distinction we need to draw is in the policy implications of this simple insight. While events have thoroughly discredited the Republicans' sloppy and simplistic tactic of making rich people richer, a smarter, more precise approach would achieve the ultimate goal of broadly shared prosperity. As I will argue in future posts, in order to do so, the left will need to reconsider its take on some of its favorite villains, including corporations and globalization.

- Dr. Martin Luther King, Jr., addressing striking sanitation workers in Memphis, March 18, 1968

The living wage movement uses MLK's words as a rallying cry to require employers to pay enough for people to get by. A noble aim, but it's an example of how a simplistic view of our role in the economy leads to self-defeating policy. Unfortunately, you shoot yourself in the foot when you target wages.

We should consider why we work in the first place: to pay for the things we need to get by. I can tell you that if everything were free, I wouldn't be a worker at all (if only!). It follows, then, that our interests as consumers should take precedence over our interests as workers, and that we are better served ensuring the adequacy of our income by focusing our efforts on reducing the cost of living rather than increasing our means to meet it. Not only would we more directly address the essential problem at hand, we would avoid the self-defeating aspect of increasing aggregate income, a scenario where the benefit of higher wages is offset by the inflationary pressure pay raises put on production expenses. Your standard of living doesn't improve if your raise is offset by price increases. Lazy people like me appreciate how this dynamic sends us in the wrong direction.

Perhaps this sounds uncomfortably similar to the supply-side economics championed by the right since the days of Reagan. Still, we can't ever let partisanship triumph over reason, and it's a valid observation that we should prefer cutting costs to raising income (if food were free, wouldn't you join me in a life of leisure?). The distinction we need to draw is in the policy implications of this simple insight. While events have thoroughly discredited the Republicans' sloppy and simplistic tactic of making rich people richer, a smarter, more precise approach would achieve the ultimate goal of broadly shared prosperity. As I will argue in future posts, in order to do so, the left will need to reconsider its take on some of its favorite villains, including corporations and globalization.

Sunday, January 8, 2012

Household debt, part III: The road ahead, or I can't drive 55

My 3rd -and for now, final - post on household debt concerns its implications on our future. If we continue on our current trajectory, it could take people a decade or more to pay down their debts to a sustainable level. Perhaps Washington will do something to help speed this up, such as enacting a more effective mortgage modification program, but I'm not holding my breath. Meanwhile, the deleveraging process places a drag on our macro growth prospects as people will need to live below their means in order to repay their debts. (As an aside, while this may seem intuitive, it's not as broadly accepted as you may think. However, this fairly readable study from the Federal Reserve Bank of San Francisco makes a compelling argument).

Despite this, I'm optimistic. While we have a huge hole to dig out of, things are actually going better than I expected. For example, the chart below depicts the portion of after-tax household income that goes to servicing debts. It should first be noted that this data is very sketchy and is useful more for trend analysis than as an absolute measure. Still, incredibly, and no doubt aided by the Fed's maintenance of extraordinarily low interest rates, households are now operating at a level not seen since the mid-90's.

I expect this to be sustainable because the employment picture has been getting better recently and the Fed has been going out of its way to set expectations that it won't touch interest rates for at least another year. These two factors could also be somewhat inflationary, which would be helpful, despite what you hear from some corners. This is because wages generally track inflation, so, since the face value of the outstanding debt is fixed, higher inflation makes it easier for people to manage their debts.

Another cause for some optimism here relates to the actual impact the deleveraging is having on our growth. This chart indicates the rate of consumption growth after inflation over the last 15 years. We only have 2011

data through November, but still what we have shows that personal spending is now growing at more or less the same rate as it was before the recession.

data through November, but still what we have shows that personal spending is now growing at more or less the same rate as it was before the recession.

Moreover, as the next chart shows, even after accounting for inflation personal spending is not only back above where it was at the start of the recession, but other than flat-lining during the "double dip" scare earlier in the year, it's been on a

pretty consistent uptrend

for a while now. When you

consider how much better

the employment picture has gotten recently, it would be reasonable to expect this trend to have legs.

the employment picture has gotten recently, it would be reasonable to expect this trend to have legs.

Economic forecasts are generally horrible (what Obama would give to be able to take back "recovery summer"!). While we can project out from current trends, unforeseeable influences will undoubtedly emerge and could easily overwhelm the status quo. Still, while we know about threats from Europe's sovereign debt crisis and China's growth deceleration, to name two of the bigger ones grabbing headlines, it's perhaps harder to predict positive surprises, such as the potential for constructive action from Washington, or the impact of the human capital upgrade as people left the labor force to go back to school. Also, growth can be self-reinforcing -in a manner equal and opposite to the recession's vicious cycle- and we may already have enough momentum to make it more difficult for bad news to derail us.

However, in the interest of full disclosure I should point out that my optimism is far from the consensus view. Many economic forecasters are predicting a slow-down in the first half of 2012, with some even expecting a recession. I don't see it in the data I'm looking at but who knows; or as Sammy Hagar once sang for Van Halen, only time will tell if we'll stand the test of time.

Despite this, I'm optimistic. While we have a huge hole to dig out of, things are actually going better than I expected. For example, the chart below depicts the portion of after-tax household income that goes to servicing debts. It should first be noted that this data is very sketchy and is useful more for trend analysis than as an absolute measure. Still, incredibly, and no doubt aided by the Fed's maintenance of extraordinarily low interest rates, households are now operating at a level not seen since the mid-90's.

I expect this to be sustainable because the employment picture has been getting better recently and the Fed has been going out of its way to set expectations that it won't touch interest rates for at least another year. These two factors could also be somewhat inflationary, which would be helpful, despite what you hear from some corners. This is because wages generally track inflation, so, since the face value of the outstanding debt is fixed, higher inflation makes it easier for people to manage their debts.

Another cause for some optimism here relates to the actual impact the deleveraging is having on our growth. This chart indicates the rate of consumption growth after inflation over the last 15 years. We only have 2011

Moreover, as the next chart shows, even after accounting for inflation personal spending is not only back above where it was at the start of the recession, but other than flat-lining during the "double dip" scare earlier in the year, it's been on a

pretty consistent uptrend

for a while now. When you

consider how much better

the employment picture has gotten recently, it would be reasonable to expect this trend to have legs.

the employment picture has gotten recently, it would be reasonable to expect this trend to have legs.Economic forecasts are generally horrible (what Obama would give to be able to take back "recovery summer"!). While we can project out from current trends, unforeseeable influences will undoubtedly emerge and could easily overwhelm the status quo. Still, while we know about threats from Europe's sovereign debt crisis and China's growth deceleration, to name two of the bigger ones grabbing headlines, it's perhaps harder to predict positive surprises, such as the potential for constructive action from Washington, or the impact of the human capital upgrade as people left the labor force to go back to school. Also, growth can be self-reinforcing -in a manner equal and opposite to the recession's vicious cycle- and we may already have enough momentum to make it more difficult for bad news to derail us.

However, in the interest of full disclosure I should point out that my optimism is far from the consensus view. Many economic forecasters are predicting a slow-down in the first half of 2012, with some even expecting a recession. I don't see it in the data I'm looking at but who knows; or as Sammy Hagar once sang for Van Halen, only time will tell if we'll stand the test of time.

Wednesday, January 4, 2012

Dirty money

Are you in the mood for some Occupy-style outrage? Let's look at this household debt chart again, highlighting the Reagan and Bush II Presidencies, eras which featured tax policy aimed at disproportionately benefiting our wealthiest:

You'll note that both periods featured rapid escalations in the growth rate of debt relative to the ability to repay it, and it's no coincidence. It's a tragic case of keeping up with the Joneses: people see their wealthier neighbors spend more, so they have to spend more so as not to lose position in the pecking order. This explanation is reinforced by the fact that the mix of who held this debt changed during this period, as the top 10% income earners actually managed to reduce their share 8% between 1989 and 2007 (source: Federal Reserve 2007 Survey of Consumer Finances). In other words, trickle down debt.

What does this mean? A friend of mine characterized it as a matter of regressive government handouts, where the rich got the clean money provided by tax cuts and the regular people got the dirty money facilitated by interest rate cuts, as both the 1980s and 2000s saw some aggressive monetary policy. A conspiracy theorist may interpret this as an attempt to repress the lower classes by inducing them into indentured servitude. The less conspiratorially-minded would point out that those rate cuts were reasonable responses to events such as the end of early 80's inflation, the 1987 and 2000 market crashes and the post-9/11 recession.

Indeed, it misses the point to seek retribution. The takeaway is simply that we shouldn't allow the politicians who still support these policies - including every GOP Presidential contender and most of their colleagues on Capitol Hill - to come within 1,000 yards of the corridors of power. You don't need a grand conspiracy theory to be concerned about the oppressive nature of carrying a high personal debt burden, or to be outraged at this result of the now-obviously ridiculous notion that making the rich richer would benefit us all.

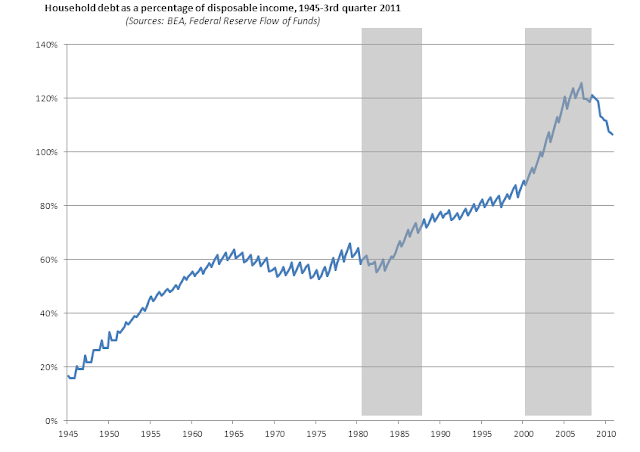

Sunday, January 1, 2012

one number to rule them all

There is already a bookshelf full of analysis picking apart the wreckage of the economic calamity to determine why it happened. Tons of blame has been passed around - incompetent or unethical bankers, Fannie & Freddie's structural flaws, unscrupulous mortgage brokers, trickle-down economics - and I don't doubt that there's some validity to all of it. To me, the debacle exposed flaws in every link of the chain.

Still, I think the whole mishegas can ultimately be boiled down to one thing: the consumer debt surge that preceded the disaster. I'll have more to say about this in future postings, including why it happened and its implications on how we move forward, but if a picture tells 1,000 words, it's worth taking a moment to consider the chart below, which depicts the debt burden of American households since WWII:

Two conclusions you can easily draw from this:

1. In retrospect, it's hard to imagine a soft landing to what built up over the last 25 years.

2. Despite the relative thriftiness of the last 3 years, we still have a long way to go.

Still, I think the whole mishegas can ultimately be boiled down to one thing: the consumer debt surge that preceded the disaster. I'll have more to say about this in future postings, including why it happened and its implications on how we move forward, but if a picture tells 1,000 words, it's worth taking a moment to consider the chart below, which depicts the debt burden of American households since WWII:

Two conclusions you can easily draw from this:

1. In retrospect, it's hard to imagine a soft landing to what built up over the last 25 years.

2. Despite the relative thriftiness of the last 3 years, we still have a long way to go.

Subscribe to:

Posts (Atom)